Why TSGLI Policy Matters More Than You Think

When I first heard about TSGLI (Telangana State Government Life Insurance), honestly, I thought it was just another “mandatory deduction” from a government employee’s salary. But as I dug deeper, I realized something shocking — this policy is not just about saving a few rupees every month; it’s a lifeline for your family’s future, a silent promise that no matter what happens, financial support will always be there.

Now think about this for a moment:

What would happen if tomorrow something unexpected occurs, and your family is left without your income? Will they have enough savings to survive? Will your children’s education continue? Will your parents or spouse be able to pay off loans? These are uncomfortable questions, but TSGLI is designed to answer them with confidence and security.

That’s why I felt it’s important to write this guide — not just to explain the technical details, but to make you truly understand why TSGLI is one of the most underrated yet powerful financial tools for Telangana government employees.

In this blog, I will walk you through every detail — eligibility, premiums, benefits, loan facility, maturity, claim process, and even how to check your policy details online. By the end, you won’t just “know” about TSGLI, you’ll appreciate it, use it wisely, and take action to secure your future.

So, if you’re a Telangana government employee or know someone who is, stay with me till the end. Because missing out on the true benefits of TSGLI could mean leaving your family financially vulnerable — and I don’t want that to happen to you.

What is TSGLI?

Before we dive into premiums, loans, and claims, let’s start with the basics.

TSGLI stands for Telangana State Government Life Insurance Scheme. It is a savings-cum-insurance scheme that has been made compulsory for all state government employees of Telangana. That means, if you are a government employee, a part of your salary is automatically deducted every month towards TSGLI.

But here’s the part many people miss:

This isn’t just a deduction. It’s an investment in two directions at once:

- Insurance Protection – Your family is financially secured in case of your unfortunate death.

- Savings & Returns – You get back the maturity value with bonuses when the policy ends.

When the scheme was introduced, the Government of Telangana had only one clear purpose in mind — to ensure that every employee, whether new or retiring soon, has a financial safety net that guarantees stability.

Now, if you compare this with taking an insurance policy from a private company, you’ll notice one big difference: TSGLI premiums are highly affordable, but the returns and benefits are guaranteed because it’s a government-backed scheme.

I personally like to call TSGLI the “silent partner” in every employee’s financial journey — you don’t actively notice it every month, but when life throws a challenge, this partner steps up and supports your family.

In simple words:

TSGLI = Protection + Savings + Government Guarantee.

And if you ask me, that combination is rare in today’s financial world.

Key Features of TSGLI Policy

When I first looked into TSGLI, what surprised me the most was how simple yet powerful its features are. Many people treat it as “just another deduction,” but when you really look closely, you realize that it’s a complete financial shield built into your salary.

Here are the standout features of TSGLI:

- Compulsory for Government Employees

Every regular Telangana State Government employee must be enrolled in TSGLI. No one is left behind. - Savings + Insurance Combo

A part of your salary acts as a savings plan (returned at maturity with bonuses) while also giving you life insurance coverage. - Affordable Premiums

Premiums are deducted directly from your salary in small, manageable amounts — making it effortless. - Loan Facility

Need urgent money? You can take a loan against your TSGLI policy at a low interest rate. - Maturity Benefits

On retirement or policy maturity, you receive your contributions back along with bonuses. - Death Benefits

In case of unfortunate death during service, the nominee receives the sum assured plus bonus, ensuring family protection. - Government Guarantee

Unlike private schemes, TSGLI is completely government-backed, meaning it’s secure and reliable.

TSGLI Policy Features at a Glance

| Feature | Details |

|---|---|

| Eligibility | All Telangana State Government Employees |

| Nature of Scheme | Savings + Life Insurance |

| Premium Payment | Compulsory monthly salary deduction |

| Loan Facility | Yes, at concessional interest rates |

| Maturity Benefit | Premiums + Bonuses on completion |

| Death Benefit | Sum assured + Bonus to nominee |

| Tax Benefits | Eligible under Section 80C of Income Tax Act |

| Safety | Fully Government-backed (100% secure) |

When you think about it, TSGLI is not just a policy, it’s a built-in financial strategy. You don’t have to make separate efforts to pay premiums, you don’t have to worry about market risks, and you don’t have to chase agents — everything happens seamlessly.

And this is where many employees miss out: they don’t even check their policy details or nominate their family members properly. That small mistake could create big problems later.

TSGLI Policy Details You Must Know

Whenever I sit with government employees and ask them about their TSGLI, most of them only say: “Yes, I know it gets deducted from my salary.” But beyond that, very few people actually know the full details. And that’s dangerous — because if you don’t know your rights and benefits, you can’t make the most out of them.

Here are the core details every employee should be aware of:

1. Eligibility Criteria

- All permanent government employees of Telangana are automatically eligible.

- Employees must be between 21 and 53 years of age to be enrolled.

- Temporary employees, work-charged, and contingent staff are generally not eligible.

👉 In short: If you are a regular Telangana State Government employee, TSGLI is compulsory for you.

2. Premium Rates

- Premiums are deducted monthly from your salary by your Drawing and Disbursing Officer (DDO).

- The amount depends on your pay scale.

- Premiums are low and fixed, yet powerful in terms of benefits.

(In the next section, I will show you an updated premium slab table so you can clearly see how much you pay and what coverage you get.)

3. Coverage and Sum Assured

- Your coverage is directly linked to your premium.

- Higher the premium, higher the sum assured.

- In case of unfortunate death, your nominee will receive Sum Assured + Bonus.

This is where the scheme really shines — unlike private policies where insurance and savings are separate, here both are bundled together.

4. Nomination Process

One of the biggest mistakes I’ve seen is that employees don’t update their nominees. Imagine this: your policy matures or you pass away, and the nominee is someone who isn’t even alive anymore, or not the right person to receive the benefit. That would create chaos for your family.

So, always:

- Fill the nomination form at the time of joining.

- Update it immediately after marriage, children, or any family changes.

- Verify with your DDO that the nominee’s details are correctly entered.

5. Tax Benefits

- Premiums paid under TSGLI are eligible for tax deduction under Section 80C of the Income Tax Act.

- The maturity amount you receive is also tax-free (under current rules).

This means you’re not just saving for the future, but also reducing your tax burden today.

Why These Details Matter

If you ignore these basics, you may end up with problems like:

- Wrong nominee → family disputes.

- Unawareness of coverage → financial shock in case of emergencies.

- Not tracking your policy → losing claim benefits.

That’s why I always tell employees: Don’t just let TSGLI run in the background. Take charge of it. Check your details, confirm your coverage, and ensure your family knows about it.

Premium Rates and Deductions under TSGLI

When I first checked my payslip, I noticed a small amount deducted under TSGLI. At that time, I didn’t bother much — but later, when I actually looked at the premium vs. benefit chart, I was shocked. The returns and coverage are far more valuable than the small deduction we often ignore.

Here’s a clear breakdown of premium rates and what they mean for you:

TSGLI Premium Slabs (Illustrative Table)

| Monthly Premium (₹) | Sum Assured (₹) | Remarks |

|---|---|---|

| 250 | 25,000 | Minimum contribution |

| 500 | 50,000 | Standard coverage |

| 750 | 75,000 | Moderate coverage |

| 1,000 | 1,00,000 | Balanced plan |

| 1,500 | 1,50,000 | Higher coverage |

| 2,000 | 2,00,000 | Popular slab |

| 3,000 | 3,00,000 | Senior officers often opt this |

| 5,000 | 5,00,000 | Maximum slab in many cases |

(Note: Exact slabs may be revised by Govt Orders (GOs). Always confirm with the latest TSGLI circular or your DDO.)

Example Calculation: How Premiums Work

Let’s say you are contributing ₹500 per month (₹6,000 annually).

- Over 20 years of service → ₹1,20,000 total premium paid.

- On maturity → You don’t just get ₹1,20,000, but also bonus + accrued benefits.

- In case of death → Your nominee gets Sum Assured (₹50,000) + bonus, which is often much higher than premiums paid.

Now think about it: Where else will you get guaranteed insurance + savings at such a low cost, without paperwork or effort?

Why Premium Awareness Matters

Most employees never even check:

- How much premium is being deducted?

- What is the corresponding sum assured?

- Have they chosen the right slab for their family’s needs?

👉 My advice: Check your payslip today. See your premium slab and compare it with your family’s future financial needs. If you feel the coverage is too low, request an enhancement of premium slab through your DDO.

Benefits of TSGLI Policy

Whenever I think about TSGLI, one thought comes to my mind: “This isn’t just insurance, it’s peace of mind packed inside a small deduction.”

Most of us don’t realize the hidden strength of TSGLI until a real-life situation comes up. That’s why I want to highlight the benefits in both practical and emotional terms.

1. Dual Advantage: Insurance + Savings

Unlike most policies where you either get savings OR insurance, TSGLI gives you both in one package.

- Your premiums build a savings corpus for maturity.

- At the same time, your family gets insurance coverage in case of death.

It’s like walking on two financial paths at once — safety for today and wealth for tomorrow.

2. Financial Security for Your Family

Imagine a situation (God forbid) where something unexpected happens to you. Would your family have enough to survive without your income?

TSGLI answers this scary question with confidence:

- Your nominee will receive sum assured + bonus immediately.

- This means no sudden financial crisis, no begging for help, no broken dreams for your children.

👉 This is where TSGLI isn’t just a policy, it’s a lifeline for your loved ones.

3. Easy and Affordable

You don’t have to remember due dates, visit offices, or pay premiums manually.

- The amount is auto-deducted from your salary.

- Premiums are small and manageable, yet the benefits are massive.

Honestly, this is one of the most effortless investments you’ll ever make.

4. Loan Facility for Emergencies

Life is unpredictable. Sometimes you may need quick money — medical emergencies, children’s education, or urgent family needs.

With TSGLI, you can take a loan against your policy at concessional interest rates. This is like borrowing money from your own savings, without begging from banks or relatives.

5. Guaranteed Returns + Bonuses

Unlike risky investments where markets go up and down, TSGLI is backed by the government.

- Your maturity value is guaranteed.

- On top of that, you earn bonuses every year, which increase your final payout.

This is where TSGLI beats many private schemes — security plus growth, without any tension.

6. Tax Benefits

The premiums you pay are eligible under Section 80C of the Income Tax Act.

This means you are saving money in two ways:

- Building a financial cushion for your future.

- Reducing your current tax burden.

7. Psychological Benefit: Peace of Mind

There’s something priceless about knowing: “Even if I’m not around tomorrow, my family will be safe.”

That mental relief, that calm sleep at night, is perhaps the biggest benefit of all.

In short, TSGLI gives you:

- Financial safety during life.

- Family protection after life.

- Effortless savings for future goals.

If you ask me, this is one of the most underrated financial blessings government employees have, but unfortunately many never even bother to explore it.

Loan Facility under TSGLI

One of the hidden gems of the TSGLI scheme is the loan facility. Many employees don’t even know that they can borrow against their policy — and at a much lower interest rate than personal loans from banks.

When I first learned about this feature, it struck me as a true life-saver. Why? Because emergencies don’t wait, and having a quick, low-interest loan option in your back pocket means you’ll never be left helpless.

How Much Loan Can You Take?

- Generally, you can take a loan up to 90% of your policy’s surrender value.

- The actual eligibility depends on your policy balance and contributions.

- The amount is sanctioned quickly compared to other loan types.

Interest Rate

- TSGLI loans usually come with a concessional interest rate (lower than market rates).

- Interest is deducted monthly along with repayment, making it easy to manage.

- Since it’s government-backed, the interest is transparent and fixed, unlike private lenders who keep changing rates.

Repayment Method

- Loan is repaid through monthly salary deductions.

- You don’t have to worry about missing payments — it’s automatic and stress-free.

- You can also repay early if you wish to clear it off.

Step-by-Step: How to Apply for a TSGLI Loan

- Visit Your DDO (Drawing and Disbursing Officer):

Collect the loan application form. - Fill in Policy Details:

Mention your policy number, deduction details, and the amount required. - Submit Required Documents:

Usually includes payslip, ID proof, and TSGLI policy passbook. - Approval Process:

DDO verifies your eligibility and forwards it to the TSGLI office. - Loan Disbursement:

Once approved, the loan is credited to your account.

Why This Loan is Better Than a Bank Loan

- No complex paperwork

- No credit score checks

- Quick approval

- Low interest rate

- Salary-based repayment

In simple words, it’s like borrowing your own money at low cost.

Whenever I think about the TSGLI loan, I see it as a safety valve — it’s not something you want to use often, but knowing it’s there gives you confidence to face life’s uncertainties.

How to Apply for TSGLI Policy

Now that we know what TSGLI is and why it’s powerful, the next logical question is: How do I apply for it?

The good news is — if you are a Telangana State Government employee, you don’t have to run around or deal with agents. The process is straightforward and mostly handled through your office.

Step-by-Step Process to Apply for TSGLI

Step 1: Approach Your Drawing and Disbursing Officer (DDO)

- TSGLI applications are managed through the DDO of your department.

- Visit your office DDO and ask for the TSGLI proposal form.

Step 2: Fill the Proposal Form

- Provide your basic details: name, employee ID, date of birth, designation, etc.

- Choose the premium slab (₹250, ₹500, ₹1000, etc.) based on how much coverage you want.

- Nominate your family member (spouse, child, parent, etc.).

Step 3: Submit Required Documents

- Proof of date of birth (SSC certificate, Aadhaar, or service register entry).

- Latest payslip.

- Identity proof.

- Nominee details with ID proof (if required).

Step 4: DDO Verification

- Your DDO will verify the details and forward the form to the TSGLI department.

- The first premium will be deducted from your next salary.

Step 5: Policy Issuance

- Once processed, you will receive a TSGLI policy bond with your policy number.

- This is proof of your enrollment and must be kept safe.

Online Services (For Policyholders)

The TSGLI department has also introduced online facilities through its official website. Some key services available are:

- Policy bond download.

- Premium details and payment history.

- Loan status and balance check.

- Maturity claim status tracking.

👉 You can visit the official site: TSGLI Official Website (external link) to explore these services.

Pro Tip (From My Personal Experience)

- Always double-check your nominee details.

- Ensure your policy number is correctly noted in your records.

- Register for online services so you don’t depend only on office staff to know your policy status.

Applying for TSGLI is simple, but the real responsibility lies in tracking it regularly. Remember, a policy ignored is as risky as not having one at all.

TSGLI Maturity & Claim Settlement Process

When the TSGLI policy reaches its maturity stage, it becomes the moment of reward for years of disciplined savings and protection. Many employees often wonder – “How will I receive my money? What steps should I follow for a smooth claim settlement?” Let’s simplify the entire process step by step.

✅ Maturity Claim Process

- Check Policy Maturity Date – Ensure that your policy term has been completed. TSGLI issues maturity value only after the stipulated term ends.

- Collect Required Documents – You’ll need:

- Filled Claim Form (available with the DDO or TSGLI office)

- Original TSGLI Bond/Policy document

- Identity proof (Aadhaar, PAN, etc.)

- Bank account details (cancelled cheque or passbook copy)

- Submit through DDO – All claims must be forwarded through the Drawing and Disbursing Officer (DDO) under whom the employee is working.

- Verification – The DDO will verify service details, premium deductions, and forward the claim to the TSGLI Directorate.

- Settlement & Payment – Once verified, the maturity amount (Sum Assured + Bonus) is directly credited to your bank account.

✅ Death Claim Process (For Nominees)

If the policyholder passes away before maturity, the nominee is eligible to receive the death claim settlement.

Steps include:

- Submission of Death Certificate

- Nominee’s ID proof & bank details

- TSGLI Policy document

- Claim Form (filled by nominee & verified by DDO)

After due verification, the death claim is settled, ensuring financial security for the family.

⚡ Key Points to Remember

- Always nominate a family member at the time of policy issuance.

- Ensure that premium deductions are updated and visible in pay slips.

- Keep the policy bond safe, as it is mandatory for settlement.

- Settlement is usually completed within a reasonable time once documents are in order.

👉 In short, TSGLI makes sure that your years of contributions don’t go in vain. Whether you’re claiming maturity benefits or your family is supported through death benefits, the settlement process is structured to provide timely financial relief.

TSGLI Tax Benefits & Exemptions

One of the biggest reasons why employees love TSGLI is not just the insurance coverage + savings, but also the tax relief it provides. Let’s decode how TSGLI helps you save extra money legally under Indian tax laws.

✅ Tax Benefits on Premium Paid

- The premium you contribute towards your TSGLI policy is eligible for tax deduction under Section 80C of the Income Tax Act, 1961.

- You can claim up to ₹1.5 lakh per year (combined limit with other 80C investments like PF, LIC, ELSS, etc.).

- This means you are not only securing your future but also reducing your present tax liability.

✅ Tax-Free Maturity Amount

- The maturity proceeds (Sum Assured + Bonus) received at the end of the policy term are fully exempt under Section 10(10D) of the Income Tax Act.

- This means the money you receive at maturity is 100% tax-free.

✅ Tax-Free Death Benefits

- In case of unfortunate death of the policyholder, the claim amount given to the nominee is also tax-free.

- Families don’t need to worry about any tax deductions on the settlement.

⚡ Why This Matters for You

Think about it: you are paying premiums → saving tax today → building wealth for tomorrow → and when you finally receive the money, it’s completely tax-free. This is a triple advantage that very few financial instruments offer.

👉 In simple terms, TSGLI is not just an insurance policy. It’s also a tax-saving, wealth-building, and family-protecting plan rolled into one.

Frequently Asked Questions (FAQs) about TSGLI Policy Details

1. What is TSGLI and who is eligible?

TSGLI (Telangana State Government Life Insurance Scheme) is a savings-cum-insurance policy designed exclusively for Telangana State Government employees. It is compulsory for all employees drawing a regular salary from the state government.

2. Is TSGLI mandatory for all employees?

Yes. As per government rules, every permanent state government employee must subscribe to TSGLI. The monthly premium is deducted automatically from their salary.

3. What is the minimum and maximum premium for TSGLI?

The minimum subscription is ₹250 per month, while higher slabs are available depending on salary and designation. There is no upper limit if you wish to contribute more.

4. What is the lock-in period for TSGLI?

The lock-in period is 3 years from the date of policy issuance. Only after this, a loan can be availed against the policy.

5. Can I take a loan against my TSGLI policy?

Yes. After completing 3 years of subscription, you can avail a loan up to 90% of the surrender value of your policy.

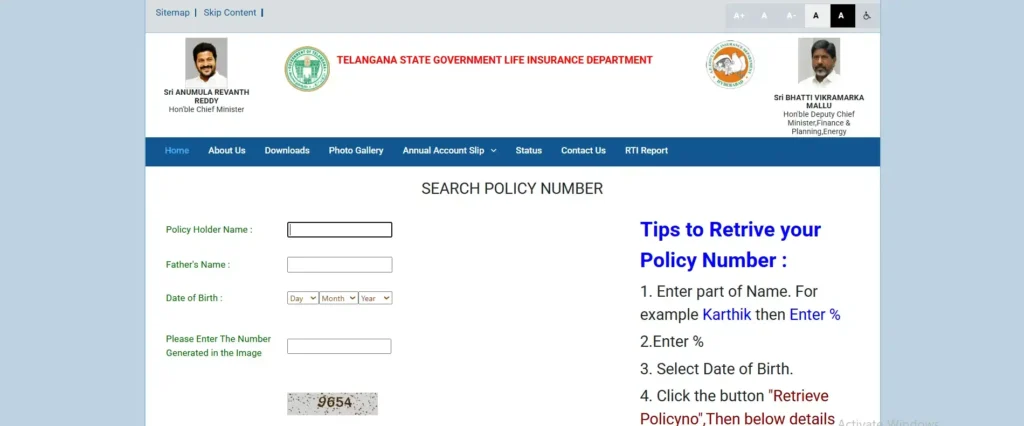

6. How do I check my TSGLI policy details online?

You can visit the official TSGLI website (http://www.tsgli.telangana.gov.in) and use your Policy Number and Date of Birth to check policy status, loan eligibility, and account balance.

7. What is the maturity period of TSGLI?

The policy matures at the end of the term opted (usually 20 years or more), after which the Sum Assured + Bonuses will be paid to the policyholder.

8. Is the maturity amount of TSGLI taxable?

No. The maturity proceeds are 100% tax-free under Section 10(10D) of the Income Tax Act.

9. What happens if the policyholder dies before maturity?

In case of unfortunate death, the Sum Assured + Bonuses will be paid to the nominee, ensuring financial security to the family.

10. Can I increase my premium contribution later?

Yes. Employees can request their DDO (Drawing and Disbursing Officer) to revise their subscription slab as per salary hikes.

11. How are claims settled under TSGLI?

Claims are settled by submitting the required documents (policy bond, death certificate in case of death claim, discharge form, etc.) to the concerned TSGLI District Office. After verification, the claim is processed and credited directly to the bank account.

12. What documents are required to apply for TSGLI?

- Filled proposal form

- Passport-size photographs

- Age proof (SSC certificate or equivalent)

- Employment details certified by the DDO

13. What is the official website for TSGLI?

The official website is TSGLI Official Portal where you can find forms, policy details, and online services.

👉 Pro Tip: Always update your nominee details in TSGLI records. In many cases, families face delays because the nominee information was outdated or missing.

Disclaimer

The information provided in this article about TSGLI Policy Details is for educational and informational purposes only. While every effort has been made to ensure accuracy, rules, benefits, and procedures under the Telangana State Government Life Insurance Scheme (TSGLI) may change from time to time as per government notifications.

Readers are strongly advised to:

- Verify the latest details from the official TSGLI website http://www.tsgli.telangana.gov.in or from their respective District Insurance Office.

- Consult with their Drawing and Disbursing Officer (DDO) or financial advisor before making any decision regarding premiums, loans, or claims.

The author is not responsible for any financial decisions made solely on the basis of this content. This article is meant to guide, simplify, and spread awareness about the scheme — not to substitute official policy documents.